Fairness and accuracy reign supreme in the dynamic and ever-evolving realm of finance. Making the evaluation of creditworthiness crucial for both lenders and borrowers. Creditors consistently seek comprehensive information to assess a borrower’s ability to meet loan commitments. Conversely, debtors undergo a somewhat opaque procedure whereby the standards for acceptance are not always apparent, thereby making it challenging to raise their creditworthiness.

Traditional credit scoring systems often fail to consider important factors that impact a borrower’s creditworthiness. This leads to the loss of valuable customers, a decline in market share, or even approving loans to the wrong individuals due to incomplete data.

But here’s where the game-changing power of Artificial Intelligence (AI) and Machine Learning (ML) comes in, revolutionizing the credit scoring landscape. With a more comprehensive approach to evaluating creditworthiness, lenders can now make better-informed decisions supported by thorough data analysis.

These cutting-edge technologies enable a more inclusive assessment of an individual’s financial behavior. By incorporating alternative data sources & finding default patterns based on customer behavior and accommodating those with limited credit history, AI systems aim to break down barriers faced by underserved populations and enhance the entire credit scoring system.This blog will explore the role of AI and Machine Learning (ML) from the credit scoring aspect.

AI-based Credit Scoring:

Credit scoring is a numerical depiction of a person’s creditworthiness based on credit history and financial behavior.

Unlike the traditional method based on historical data and fixed variables, artificial intelligence-based credit scoring makes use of machine learning algorithms to examine a large volume of data from numerous sources. This sophisticated method forecasts the loan payback capability of a borrower. AI-driven credit scoring offers a complete evaluation of credit risk, thereby giving lenders precise and diverse information on a borrower’s financial behavior.

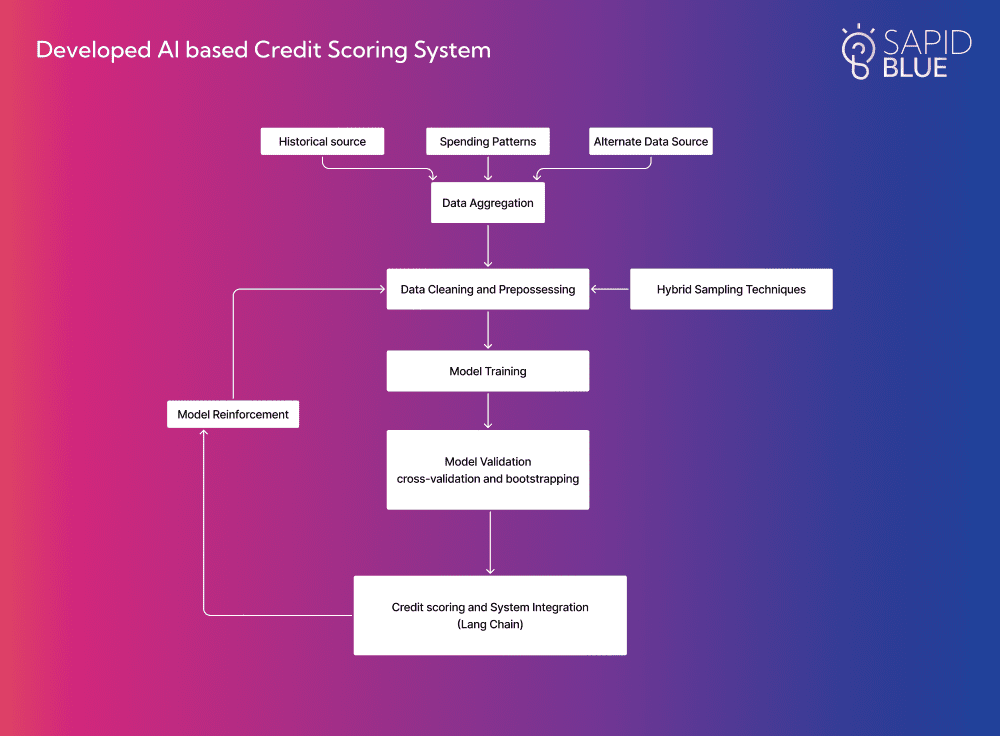

Artificial intelligence has revolutionized credit scoring by harnessing the power of machine learning models. Allowing systems to learn from historical data, enabling them to evaluate the creditworthiness of borrowers with precision. The process begins with data aggregation, where AI-driven credit scoring systems gather information from various sources, including traditional credit data, patterns and alternative data. This comprehensive view of an individual’s financial behavior forms the foundation for analysis.

Machine learning algorithms then dive into this preprocessed dataset, uncovering intricate patterns and dependencies that influence credit risk. By identifying the features that have the greatest impact on predicting a borrower’s repayment capacity, these algorithms fine-tune their models. Once trained, these models can accurately predict outcomes for new data, such as evaluating loan applications based on historical patterns gleaned from past borrower behaviors.

Data Cleaning and Processing

Developing AI-powered credit scoring systems requires a strong focus on data. Providers must guarantee the suitability and impartiality of the data used for training, testing, and validation. This involves meticulously documenting the data’s type, origin, number of data points, and the methodologies employed for data curation, including cleaning and filtering. Additionally, ensuring transparency and reliability in the AI system necessitates considering the computational resources needed for model training and estimating energy consumption.

Hybrid Sampling Techniques

To improve model accuracy, hybrid sampling techniques, such as the SMOTEENN (Synthetic Minority Over-sampling Technique combined with Edited Nearest Neighbors), are employed. This method incorporates both oversampling and undersampling strategies to address imbalances in the dataset, ensuring the model is trained on a more representative sample of borrowers

Model Training

The model identifies patterns and relationships indicating credit risk and refines predictions by recognizing significant features impacting repayment capacity. Once trained, the model accurately evaluates new loan applications by comparing them against learned patterns.

Model Validation

Model validation is a crucial step in AI-based credit scoring. It ensures the accuracy and reliability of the predictive model. To achieve this, the trained model is tested on a separate dataset that was not used during training. The objective is to assess how well the model performs on new, unseen data. Data scientists employ key metrics such as accuracy, precision, recall, and the area under the receiver operating characteristic (ROC) curve to evaluate the model’s performance. By comparing these metrics against predefined benchmarks, they can determine if the model is robust and reliable.

Moreover, techniques like cross-validation and bootstrapping are utilized to further validate the stability and generalizability of the model. These additional methods enhance confidence in the model’s performance and its ability to make accurate predictions in real-world scenarios.

Systematic Integration of AI Components and Deployment

Advanced AI systems can leverage frameworks like LangChain to seamlessly integrate different AI components, ensuring smooth processing workflows. To kickstart document processing, the inclusion of technologies such as Python and OCR (Optical Character Recognition) libraries is crucial. These technologies enable efficient extraction of text from intricate financial documents.

Benefits of AI and Machine Learning in Credit Scoring

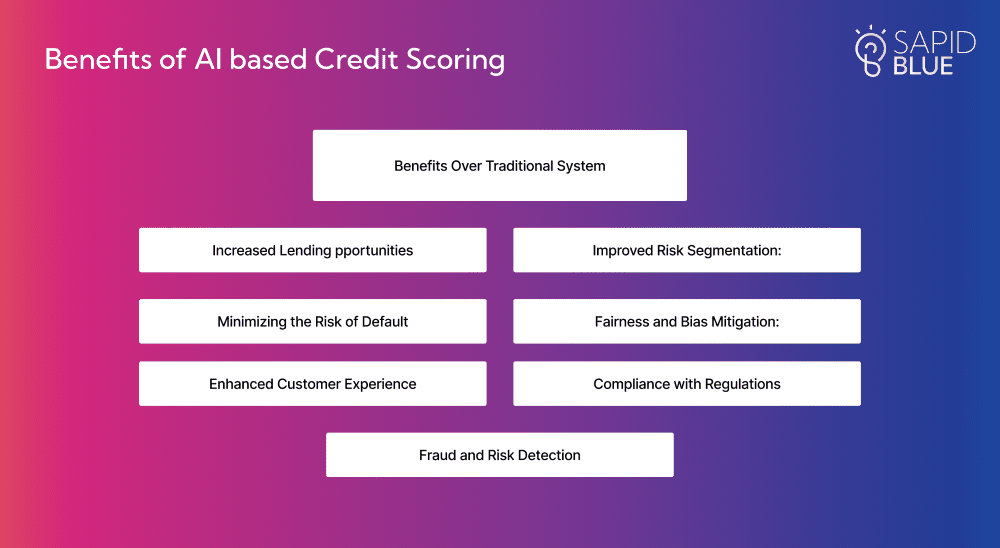

Benefits of AI-Based Credit Scoring

AI and ML-powered credit scoring systems analyze vast datasets and identify patterns to improve accuracy and support real-time decision-making. Here are some noteworthy benefits of incorporating these advanced technologies in credit scoring.

Increased lending opportunities: AI and machine learning can enable lenders to find creditworthy applicants that conventional rating systems might have missed.

Minimizing the risk of default: AI and machine learning can assist lenders in reducing loan default risk through higher credit risk assessment accuracy.

Enhanced customer experience: Faster and more effective credit approvals help to enhance the general consumer experience.

Compliance with regulations: AI can enable banks to follow consumer protection and fair lending regulations

Fraud and risk detection: AI-ML-driven systems can highlight unusual trends and fraudulent activities, thus facilitating risk management professionals to raise alerts in advance.

Improved Risk Segmentation: With AI, lenders can now accurately assess and cater to the unique needs and circumstances of each borrower, ensuring a fair and personalized lending experience.

Fairness and Bias Mitigation: Fairness is crucial in credit scoring, particularly regarding biases that can perpetuate inequalities. AI systems like BRIO aim to ensure equitable treatment for all groups. Continuous monitoring and assessment are essential to mitigate bias risks, as mandated by regulatory guidelines in the financial sector.

Why Should You Engage with AI Consulting Firms?

Working with leading AI consulting companies or blockchain consulting services can help you customize these technologies to match your specific requirements.

Companies focused on financial software development can also assist you in incorporating artificial intelligence models into your current setup. This will make your credit scoring procedure more efficient and increase the accuracy of credit assessments.

Real World Implementations (Case Studies)

Enhanced Risk Assessment

(Using unconventional data sources such as social media activity and transaction histories.)

One significant case study highlights the integration of machine learning algorithms by a major financial institution. By employing advanced data processing techniques, the institution improved its ability to analyze vast datasets, including unconventional data sources such as social media activity and transaction histories. This approach enabled more granular risk assessments, ultimately allowing the bank to extend credit to previously underserved populations while managing default risks more effectively

Governance and Oversight Mechanisms

In another example, a fintech startup adopted a robust governance model to manage its AI-driven credit scoring system. This model included comprehensive internal oversight and regular audits to ensure compliance with legal standards, particularly regarding data privacy and ethical use of information. The implementation of human oversight measures and a detailed evaluation strategy helped mitigate risks associated with algorithmic bias, thus promoting fairness in lending practices

Real-time Credit Monitoring

A prominent case study also involves a credit bureau that developed a real-time AI monitoring system for existing loans. This system continuously evaluates borrower behavior and market conditions to adjust credit scores dynamically. The technology provided timely alerts for potential risks, allowing lenders to proactively manage accounts and reduce defaults. Such innovations showcase the potential for AI to transform traditional credit scoring into a more responsive and adaptive framework

Challenges and Limitations

Despite the successes, several challenges have emerged. For instance, concerns regarding transparency and explainability in AI-driven models are significant. A study revealed that borrowers often struggle to understand how their credit scores are calculated, raising issues of trust and compliance with regulatory standards. Therefore, providers are urged to enhance their communication strategies, ensuring that information related to scoring methodologies is clear and accessible

Key Takeaways:

The credit scoring sector is being transformed by artificial intelligence and machine learning. Using these technologies can help financial institutions increase their profitability, improve customer experiences, and make financing decisions through data-driven analysis.

So, without waiting any longer, get in touch with us and take your first step towards a smarter credit scoring process.

AI Engineer | Generative AI & Computer Vision Specialist

Saurabh Sinha is an AI Engineer specializing in Generative AI, Large Language Models (LLMs), Computer Vision, and scalable AI system development. With hands-on expertise in building real-world AI applications, he has worked extensively on intelligent automation systems, YOLO-based detection and tracking pipelines, RAG architectures, vector databases, and cloud-deployed AI solutions.

Artificial intelligence has revolutionized credit scoring by harnessing the power of machine learning models. Allowing systems to learn from historical data, enabling them to evaluate the creditworthiness of borrowers with precision. The process begins with data aggregation, where AI-driven credit scoring systems gather information from various sources, including traditional credit data, patterns and alternative data. This comprehensive view of an individual’s financial behavior forms the foundation for analysis.

Machine learning algorithms then dive into this preprocessed dataset, uncovering intricate patterns and dependencies that influence credit risk. By identifying the features that have the greatest impact on predicting a borrower’s repayment capacity, these algorithms fine-tune their models. Once trained, these models can accurately predict outcomes for new data, such as evaluating loan applications based on historical patterns gleaned from past borrower behaviors.

Artificial intelligence has revolutionized credit scoring by harnessing the power of machine learning models. Allowing systems to learn from historical data, enabling them to evaluate the creditworthiness of borrowers with precision. The process begins with data aggregation, where AI-driven credit scoring systems gather information from various sources, including traditional credit data, patterns and alternative data. This comprehensive view of an individual’s financial behavior forms the foundation for analysis.

Machine learning algorithms then dive into this preprocessed dataset, uncovering intricate patterns and dependencies that influence credit risk. By identifying the features that have the greatest impact on predicting a borrower’s repayment capacity, these algorithms fine-tune their models. Once trained, these models can accurately predict outcomes for new data, such as evaluating loan applications based on historical patterns gleaned from past borrower behaviors.