Introduction

AI in credit risk management is redefining the financial landscape, offering innovative solutions to challenges faced by financial institutions, particularly to microfinance institutions where traditional approaches often struggle with managing diverse portfolios spread across diverse geographies, and limited data—making these methods time-consuming, less accurate, costly and overall in-efficient in long run.

Seeing these diverse challenges, AI in banking and finance have emerged as new solutions, where AI and Machine Learning (ML) are addressing these issues by leveraging advanced algorithms that analyze vast amounts of data to help uncover intricate patterns, and deliver highly accurate predictions. AI-powered systems automate risk assessments, enabling faster, more precise, and cost-effective decision-making. Unlike conventional models, AI excels in identifying complex relationships between macroeconomic trends and individual financial behaviour, significantly improving forecasting accuracy.

The benefits of adopting AI for credit risk management are substantial: enhanced operational efficiency, reduced risk exposure, and significant cost savings. With the global AI market in banking projected to grow from $160 billion in 2024 to $300 billion by 2030, the role of AI in credit risk management is undeniable. As financial institutions, particularly in microfinance, work towards driving financial inclusion, AI is poised to become a cornerstone for ensuring long-term sustainability and success. So let’s dive deeper into exploring AI for credit risk management.

Application of AI in Banking and Finance

AI has become an essential component of microfinance banking, with many industry leaders integrating its capabilities into their institutions. Let’s explore how AI based credit risk management, customer retention and credit inclusion works, by diving deeper into its use cases and advantages:

AI-Based Fraud Detection and Cybersecurity

By leveraging machine learning, organizations can proactively detect fraudulent activities, identify system vulnerabilities, minimize risks, and enhance the security of digital transactions.

A standout example is Danske Bank, Denmark’s largest bank, which implemented an advanced fraud detection algorithm powered by deep learning. This solution enhanced the bank’s fraud detection accuracy by 50% while reducing false positives by almost 60%. Additionally, it automated critical decision-making processes, routing complex cases to human analysts for detailed review.

Similarly, JPMorgan Chase employs AI to analyze vast amounts of transaction data in real time, identifying anomalies and potential fraudulent activities across its global operations. By integrating AI based fraud detection systems, the bank has improved fraud prevention rates and reduced manual intervention for routine checks, allowing its team to focus on high-risk cases.

The Need for AI in Fraud Detection

AI’s role in cybersecurity is particularly critical as financial institutions remain prime targets for cyberattacks. The International Monetary Fund’s Global Financial Stability Report 2024 reveals that cyber incidents in the financial sector have more than doubled. Additionally, the report from World Economic Forum highlights that nearly 20% of all cyber risks now impact financial institutions.

As financial entities increasingly adopt AI in banking and finance, its integration into fraud detection not only fortifies cybersecurity but also supports broader risk management and operational efficiency goals.

AI-Driven Personalization and Enhanced Customer Experience

By leveraging statistical models, AI-driven tools help anticipate customer needs, optimize interactions, and build stronger, long-lasting relationships.

A notable example is Amazon, which utilizes AI to power its recommendation engine. This technology analyzes customer behavior, purchase history, and browsing patterns to suggest products tailored to individual preferences. This approach has significantly increased customer satisfaction and boosted sales, demonstrating how personalized experiences can drive loyalty and growth.

Similarly, HSBC utilizes AI-driven chatbots to handle routine queries, such as account balances and transaction histor’ies. By automating these processes, the bank provides quicker resolutions and reduces wait times for high-priority customer concerns, creating a smoother overall experience.

Impact of AI on Customer Experience

AI’s transformative impact extends across e-commerce, travel, retail, and other industries, where personalized interactions and AI in customer service are becoming the norm. A 2024 report by McKinsey & Company highlights that companies implementing AI-driven personalization experience a 30% increase in customer retention rates and a 20% rise in revenue.

As customer expectations continue to evolve, AI in financial software development and AI in customer service remains a vital tool for businesses striving to deliver consistent, efficient, and personalized experiences across touchpoints. From streamlining support workflows to offering tailored recommendations, AI in finical software developemnt enhances engagement and satisfaction, enabling businesses to stay ahead in a rapidly evolving market. This trend underscores the importance of integrating AI in banking, finance, and beyond to remain competitive.

AI-Powered Credit Data Extraction and Management

AI-powered tools are transforming credit data management by enabling organizations to automatically extract, organize, and leverage critical information from multiple global and local credit agencies. This automation enhances operational efficiency, supports better decision-making, and reduces manual workload.

A standout example is Moody’s Analytics CreditLens Platform, which leverages AI to analyze credit data, financial statements, and risk factors from diverse sources. By centralizing this information, the platform provides credit teams with actionable insights to streamline assessments and improve decision-making. According to PwC, automating credit data extraction can enhance operational efficiency by up to 40%, significantly boosting productivity.

Similarly, SAP’s Credit Management Module integrates AI to streamline credit data processing. By connecting directly with credit bureaus, the system automatically updates customer credit profiles, flags high-risk accounts, and provides actionable insights for AI in credit risk management. This real-time approach empowers finance teams to make faster, data-driven decisions while minimizing errors.

Similarly, Financial institutions are also leveraging AI for credit data automation. For instance, HSBC uses AI-driven tools to pull credit reports for loan applications, reducing processing time and enhancing customer satisfaction. This automation accelerates credit approvals while ensuring compliance with regulatory standards.

Need for AI in Credit Data Management

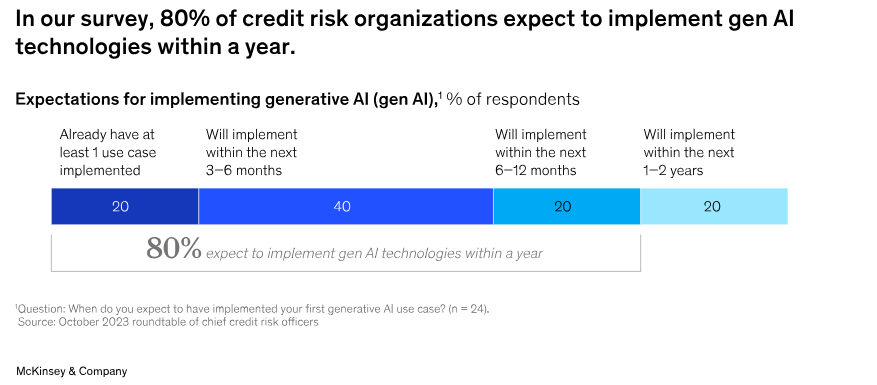

AI’s role in credit data extraction underscores its broader impact on financial operations. A recent study by Mckinsey reveals that 80% of organizations plan to implement genAI within a year. These improvements highlight the importance of adopting AI in credit workflows to streamline processes and ensure smarter, faster decisions.

By integrating AI-powered credit data management tools, businesses across industries can enhance global operations, improve compliance, and optimize credit workflows, staying ahead in a competitive landscape.

AI-Driven Automated Credit Scoring and Approval Workflow

AI based credit scoring is revolutionizing credit evaluation processes, enabling businesses to quickly and accurately assess creditworthiness. By leveraging advanced algorithms and predefined criteria, organizations can streamline decision-making, enhance consistency, and minimize manual intervention.

FinTech platforms are utilizing automated credit scoring to improve efficiency. For instance, Upstart, a leading digital lending platform, employs AI algorithms to assess non-traditional factors such as education, employment history, and income stability. This innovative approach has expanded credit access while maintaining low default rates, showcasing the transformative potential of AI based credit scoring in reimagining credit evaluations.

Similarly, Santander Bank uses automated credit scoring to evaluate small business loan applications. By integrating AI models with its approval workflows, the bank delivers faster loan decisions, improving customer experience and operational efficiency.

In microfinance, India-based CreditMantri leverages AI based credit scoring tools to evaluate underserved segments. These tools analyze alternative data sources, such as utility payments and mobile usage, to assess creditworthiness, enabling financial inclusion for customers who lack traditional credit histories.

The Impact of AI-Driven Credit Scoring

A pwc report highlights that automated credit scoring improves approval accuracy by up to 35% compared to traditional systems and reduces processing time. Furthermore, integrating these systems with collaborative workflows ensures consistent credit decisions across customer segments and geographies.

As businesses increasingly adopt AI-driven automated credit scoring and approval workflows, they can streamline credit operations, expand access to credit, and implement robust risk management practices. This underscores the growing importance of AI in financial software development to deliver innovative and efficient credit solutions.

AI-Powered Real-Time Credit Risk Monitoring

By providing continuous oversight of customer portfolios, organizations can proactively address risks and reduce the likelihood of defaults.

Financial institutions like Citibank have adopted real-time credit monitoring to enhance risk management. By analyzing vast datasets of customer transactions and external financial reports, Citibank’s AI-driven system identifies early warning signs of financial instability, allowing teams to adjust credit limits or restructure loans before defaults occur.

In the manufacturing sector, General Electric leverages AI-powered monitoring tools to manage the credit risks of its global supply chain. By continuously tracking supplier credit ratings and payment behaviors, GE ensures business continuity and minimizes exposure to financial vulnerabilities.

SME-focused platforms like Kabbage also benefit from AI-driven real-time credit monitoring. The platform uses machine learning algorithms to track cash flow patterns and external credit events, enabling tailored credit solutions while minimizing risk exposure.

The Impact of Real-Time Monitoring

A report by Deloitte highlights that organizations using AI-powered real-time credit monitoring have reduced default rates by up to 30%. This improvement reflects the effectiveness of leveraging explainable AI in credit risk management for predictive insights and faster decision-making.

As real-time credit monitoring becomes an industry standard, businesses can ensure smarter risk mitigation, optimize credit operations, and foster more stable financial ecosystems. This trend reinforces the importance of adopting AI in credit risk management to maintain resilience in a dynamic financial landscape.

AI-Enhanced Compliance and Reporting

AI-powered solutions are revolutionizing compliance and reporting processes, enabling organizations to navigate regulatory requirements with greater accuracy and efficiency. By automating data collection, analysis, and reporting, businesses can ensure compliance, reduce manual workloads, and minimize risks.

A notable example is HSBC, which leverages AI-driven tools to automate regulatory reporting across its global operations. By integrating AI with its compliance systems, HSBC ensures timely submissions, reduced errors, and thus staying ahead of complex regulatory changes in diverse markets. This demonstrates the transformative role of AI in banking and finance, enhancing transparency while significantly improving operational efficiency.

Similarly, healthcare organizations like UnitedHealth Group utilize AI to streamline compliance with data privacy regulations such as HIPAA. Advanced algorithms analyze patient records to detect anomalies, monitor data access, and generate automated reports, ensuring adherence to stringent privacy standards.

PwC’s Risk Assurance division uses AI-powered tools to assist clients in automating compliance processes. These tools analyze vast datasets to identify potential compliance breaches, flag high-risk transactions, and generate audit-ready reports, minimizing the likelihood of regulatory penalties.

The Impact of AI on Compliance and Reporting

A 2024 report by Gartner reveals that organizations adopting AI for compliance and reporting have seen a 35% reduction in regulatory penalties and a 25% improvement in reporting accuracy. These results underscore the growing importance of AI in financial software development for addressing regulatory complexities efficiently.

With AI-enhanced compliance and reporting tools, organizations can confidently navigate regulatory landscapes, maintain operational continuity, and build stronger stakeholder trust. By integrating these technologies, businesses can focus on strategic growth while ensuring robust governance frameworks.

AI-Powered Predictive Analytics for Future Trends

AI-powered predictive analytics is revolutionizing credit risk management by enabling organizations to forecast trends and identify potential risks before they occur. By analyzing historical data and uncovering patterns, these systems provide actionable insights, enhancing decision-making and reducing financial exposure.

A prominent example is the microfinance institution CreditAccess Grameen, which employs AI-driven predictive analytics to evaluate borrower risk in underserved rural areas. By analyzing repayment histories, local economic conditions, and alternative data such as agricultural cycles, the organization anticipates default risks and provides tailored repayment plans. This proactive approach fosters financial inclusion while ensuring portfolio stability.

FinTech companies like SoFi also leverage predictive analytics to enhance lending operations. By evaluating non-traditional data sources such as social media activity, education history, and job stability, SoFi’s AI models forecast default probabilities with remarkable accuracy, ensuring responsible lending practices.

In the energy sector, Shell applies predictive analytics to assess the credit risk of corporate clients. By integrating AI with its financial systems, Shell forecasts future trends in customer financial health, enabling better contract negotiations and safeguarding revenue streams.

The Impact of Predictive Analytics

Major organizational reports state that utilizing predictive analytics in credit risk management achieves up to 50% higher accuracy in forecasting potential risks. This enhanced precision allows businesses to adapt strategies, optimize credit policies, and strengthen financial stability.

By adopting AI-driven predictive analytics, companies can stay ahead of emerging risks, enhance AI-based credit scoring, and ensure more resilient financial planning in dynamic market environments. These tools empower organizations to create robust credit operations and mitigate risks effectively.

Revamping AI in Credit Risk Management with SapidBlue: A Case Study Analysis

Overview: In today’s fast-paced business environment, effective credit risk management is crucial for large enterprises to maintain financial stability and growth. SapidBlue, a leader in AI-driven solutions, recently helped a global enterprise transform its credit risk management processes. By implementing advanced AI-powered tools, SapidBlue significantly enhanced the client’s ability to assess credit risk, improve compliance, and predict future trends.

Success Story 1: Streamlined Credit Decision-Making

Client Profile: Our client, a Fortune 500 company with over $12 billion in annual revenue, faced challenges in managing credit risk efficiently across various geographies. They required a comprehensive solution to integrate data from multiple sources and automate credit decisions.

Solution: SapidBlue implemented an AI based credit risk management system that integrated data from credit bureaus, financial statements, and customer payment histories. This system used machine learning algorithms to analyze data and generate a risk score for each customer.

Results:

- Reduced Decision Layers: The approval process for credit limits was significantly streamlined. The average number of approval layers dropped from nine to four, eliminating unnecessary steps and expediting decision-making.

- Improved Cash Flow: Faster and more accurate credit decisions led to reduced credit risk and improved cash flow. This efficiency enabled the client to allocate resources more effectively.

Key Takeaway: By integrating AI-powered solutions, the client achieved a more agile and accurate credit risk management process, enhancing overall financial health.

Success Story 2: Automated Credit Management Processes

Client Profile: Another client, an American chemical manufacturer, needed to automate their credit management processes to maximize profitability and maintain consistency in credit reviews.

Solution: SapidBlue introduced a machine learning-driven credit risk management system that automated the analysis of customer data and identified high-risk patterns. The system also provided real-time alerts for changes in customers’ risk profiles.

Results:

- Paperless Operations: The client transitioned to a 100% paperless credit review process, ensuring consistency and efficiency.

- Proactive Risk Mitigation: Real-time monitoring allowed the client to make proactive decisions, significantly reducing the risk of defaults.

Success Story 3: Automated Document Review and Management Processes

Client Profile: A leading global oil and gas institute struggled with inefficiencies in managing documents and ensuring security compliance across various regions. Their existing system was hindered by fragmented data and cumbersome approval workflows, making it challenging to maintain streamlined operations.

Generative AI Solution: SapidBlue deployed an advanced AI-powered Knowledge Center that integrated various data sources, including regulatory documents, compliance reports, and security protocols. Equipped with generative AI and a live question-answer feature, the system allowed for seamless document management and real-time security compliance checks. The AI-powered platform not only facilitated faster access to critical information but also provided intelligent, automated responses to compliance queries.

Result:

- Streamlined Document Management: The AI system consolidated fragmented data, significantly simplifying document management and reducing time spent searching for critical information.

- Enhanced Compliance: Real-time security compliance checks and AI-driven insights helped the organization stay ahead of regulatory requirements and minimize risks.

- Improved Operational Efficiency: The integration of AI accelerated decision-making and operational processes, enhancing overall agility and reducing manual effort in managing complex data.

Key Takeaways

- Enhanced Compliance and Reporting

- Predictive analytics for Future Trends

- Speed and Efficiency

- Fraud Detection

- Customer Experience

Conclusion: SapidBlue’s AI-powered solutions transformed the client’s credit risk management by enhancing compliance, accuracy, speed, and predictive capabilities. These advancements not only improved operational efficiency but also positioned the client for future growth and stability.

Steps to Become AI-First Micro-Finance Institute

Artificial Intelligence (AI) has immense potential to transform the microfinance industry, enabling institutions to serve underbanked populations more efficiently, minimize risks, and drive sustainable growth. Transitioning to an AI-first microfinance institution requires a well-defined roadmap, substantial resource allocation, and a data-driven approach.

Understanding the Role of AI in Microfinance

AI in microfinance can address key challenges like:

- Risk Assessment: AI based credit scoring models analyze alternative data (e.g., mobile usage, social behavior) for accurate loan evaluations.

- Operational Efficiency: Automation of repetitive tasks reduces costs and human errors.

- Customer Engagement: Chatbots and predictive analytics enhance client interaction and satisfaction.

- Fraud Detection: Machine learning algorithms identify patterns to prevent fraudulent activities.

Steps to Become an AI-First Microfinance Institution

Step 1: Define Goals and Vision

- Establish a clear vision for leveraging AI (e.g., improving financial inclusion, reducing operational costs).

- Set measurable KPIs such as reduced non-performing loans (NPLs), improved loan approval turnaround time, or customer satisfaction scores.

Step 2: Assess Readiness

- Conduct a gap analysis to evaluate current technological capabilities, data availability, and staff expertise.

- Assess existing processes for AI integration, like loan underwriting or customer acquisition.

Step 3: Invest in Data Infrastructure

- Build or upgrade a robust data management system to collect, clean, and store diverse datasets.

- Develop policies for ethical data usage and customer privacy compliance.

Step 4: Acquire and Implement AI Technologies

- Identify suitable AI applications for risk assessment, fraud detection, and customer management.

- Partner with AI solution providers or develop in-house capabilities.

- Adopt scalable platforms to support growth.

Step 5: Train Workforce

- Provide training programs for staff to enhance AI literacy and operational adaptability.

- Hire AI specialists, data scientists, and machine learning engineers.

Step 6: Pilot AI Solutions

- Start with small-scale implementations to test AI models.

- Use A/B testing to compare AI-driven processes with traditional ones.

Step 7: Scale Up

- Gradually roll out AI-driven systems across all branches or operational areas.

- Continuously refine AI models using feedback and performance metrics.

Step 8: Monitor and Optimize

- Establish real-time monitoring dashboards.

- Regularly update AI systems to align with evolving market needs and regulatory frameworks.

Roadmap to Become AI-FIRST

| Phase | Timeline | Key Activities |

|---|---|---|

| Foundation | 0-1 months | Assess readiness, define AI goals, invest in data infrastructure, and set ethical policies. |

| Development | 6-12 months | Implement AI solutions (e.g., chatbots, credit scoring models), and conduct pilot tests. |

| Scaling | 12-15 months | Scale successful pilots, integrate AI into all operations, and ensure staff upskilling. |

| Optimization | Ongoing | Monitor performance, update models, and explore advanced AI applications like predictive modelling. |

Resources Required

Technical Resources

- Cloud Infrastructure: For scalable storage and computing power (e.g., AWS, Google Cloud).

- AI Tools: TensorFlow, PyTorch, and specialized financial analytics software.

- APIs for Alternative Data: Partner with telecom companies, social platforms, and utility providers for data access.

Human Resources

- AI Experts: Data scientists, AI developers, and business analysts.

- Training Modules: Internal workshops or partnerships with educational institutions for workforce upskilling.

Financial Resources

- Budget allocation for technology procurement, data acquisition, and training.

- External funding options (e.g., development grants, venture capital).

Partnerships

- Collaborate with AI startups, fintech companies, and academic researchers.

- Leverage global initiatives promoting financial inclusion through AI.

Challenges of Implementing AI in Banking and Fiance

While AI based credit risk management offers numerous advantages, large enterprises must navigate several potential challenges and considerations when implementing these solutions. Key issues include data privacy, ethical concerns, regulatory compliance, and technical hurdles.

Data Privacy

Data privacy is a critical concern, as large enterprises handle substantial amounts of sensitive customer information. Ensuring that any AI-powered solution complies with data privacy regulations such as the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) is paramount. For instance, a breach of GDPR can result in fines of up to €20 million or 4% of the annual global turnover, whichever is higher.

Ethical Concerns

Ethical considerations are vital when deploying AI based credit risk management solutions. These systems have the potential to automate decision-making processes, which could unintentionally introduce biases. To mitigate this, enterprises should adopt ethical AI practices, ensuring transparency in how AI systems make decisions and addressing biases in the data and algorithms. A notable example is the AI ethics guidelines proposed by the European Commission, emphasizing fairness and accountability.

Regulatory Compliance

Compliance with relevant regulations such as the Fair Credit Reporting Act (FCRA) and the Equal Credit Opportunity Act (ECOA) is essential. These laws ensure that AI-powered credit decisions are fair and non-discriminatory. Non-compliance can lead to significant legal repercussions and damage to reputation. For example, violations of the ECOA can result in penalties and corrective actions mandated by regulatory authorities.

Technical Challenges

Implementing AI based credit risk management solutions may require significant investment in new infrastructure and systems. Enterprises must ensure they have the necessary skills and expertise in-house to implement and maintain these solutions. This includes training staff on new technologies and possibly hiring specialized personnel. A case in point is JP Morgan’s investment in AI infrastructure to enhance their credit risk management capabilities.

Regular Audits and Updates

To maintain the effectiveness and compliance of AI systems, enterprises must perform regular audits and updates. This involves continuously monitoring the AI models, validating their performance, and ensuring they adapt to new regulatory requirements and market conditions. IBM’s continuous monitoring framework for AI systems serves as a good reference for maintaining AI integrity.

How SapidBlue Can Help You Become AI First

At SapidBlue, we understand that transitioning to an AI-first strategy requires more than just technology—it demands agility, scalability, and alignment with business goals. That’s why we’ve developed digital accelerators, modular and customizable “Lego building blocks” designed to fast-track your AI adoption journey.

Our approach combines cutting-edge technology with deep industry expertise to empower microfinance institutions (MFIs) to harness AI effectively and sustainably.

What Are SapidBlue’s Digital Accelerators?

Our digital accelerators are pre-built, modular components that address specific operational and strategic challenges. These are designed for rapid deployment, seamless integration, and scalability.

Key Features:

- Plug-and-Play Capability: Quick integration into existing systems.

- Customization: Tailored to align with your organizational needs.

- Scalability: Modular design allows for phased adoption.

- Efficiency: Reduces time-to-value by leveraging proven AI solutions.

How SapidBlue Supports Your AI-First Transformation

Step 1: Define and Align Objectives

SapidBlue works with you to align AI goals with your institutional mission, whether it’s enhancing financial inclusion, improving operational efficiency, or minimizing risks.

Step 2: Deploy Data-Driven Foundations

Our accelerators streamline the transition from traditional systems to AI-ready infrastructure:

- Data Integration Modules: Aggregate and clean data from diverse sources like mobile usage, credit history, and social media.

- Ethical Data Management: Ensure compliance with privacy and regulatory standards.

Step 3: Empower Risk Management

SapidBlue’s accelerators for credit risk assessment enable accurate evaluations by integrating AI models trained on alternative and traditional data.

- Pre-trained AI Models: Ready-to-use credit scoring algorithms.

- Fraud Detection Tools: Detect anomalies using machine learning techniques.

Step 4: Automate Operations

- AI-Powered Process Automation: Replace manual workflows with AI-driven automation to reduce errors and improve productivity.

- Chatbot Integration: Deploy multilingual AI chatbots for 24/7 customer support.

Step 5: Enhance Customer Experience

Leverage accelerators for personalized engagement and predictive analytics:

- Customer Segmentation Tools: Target specific demographics with tailored financial products.

- Loan Predictive Analytics: Predict repayment likelihood and optimize loan terms.

Step 6: Upskill Teams with AI Literacy

- Training Accelerators: Equip staff with the knowledge to operate and maximize AI tools.

- Interactive Dashboards: Simplify AI outputs for non-technical users.

Step 7: Continuous Optimization

SapidBlue provides accelerators for ongoing monitoring and improvement:

- AI Performance Dashboards: Real-time insights into model performance and business impact.

- Model Update Pipelines: Ensure algorithms stay relevant as market dynamics evolve.

Advantages of Using SapidBlue’s Digital Accelerators

- Speed.

- Affordability

- Flexibility

- Expertise

| Phase | Timeline | Key Activities with SapidBlue |

|---|---|---|

| Discovery | 0-15 days | Conduct workshops to define goals, assess readiness, and select accelerators. |

| Foundation | 15-30 days | Deploy data integration and risk assessment accelerators. |

| Implementation | 3-5 months | Scale AI solutions for automation, customer engagement, and fraud detection. |

| Scaling | 5-7 months | Expand AI adoption to all branches and enhance workforce capabilities. |

| Optimization | Ongoing | Use monitoring accelerators for continuous performance improvements. |

The Future of AI-based Credit Risk Management: Partnering with SapidBlue

The future of credit risk management is being transformed by autonomous AI systems, and at SapidBlue, we are at the forefront of this revolution. Our AI-powered solutions are designed to empower your enterprise with faster, more accurate, and objective decision-making capabilities, particularly in AI in credit risk management. By leveraging AI for credit risk management, our systems analyze vast amounts of data in real-time, ensuring that your credit decisions are both swift and precise, free from human bias.

With AI-based credit scoring and AI in banking and finance, our solutions not only provide consistent and objective outcomes but also continuously learn and improve, adapting to new data over time. This continuous improvement ensures that your credit risk management system remains at the cutting edge, providing more accurate and reliable results as it processes more information.

SapidBlue’s explainable AI in credit risk management further ensures transparency, allowing you to trust the automated decisions while maintaining regulatory compliance. As your enterprise navigates the complexities of credit risk, our AI solutions help you stay ahead of the curve, empowering your business to thrive in an increasingly data-driven world. Let us help you unlock the future of credit risk management, ensuring superior outcomes with confidence and ease.

FAQS

1. How does AI improve credit risk assessment in microfinance?

AI leverages machine learning models to analyze diverse data points, such as transaction histories, social behavior, and alternative credit data. This allows microfinance institutions to assess borrowers’ creditworthiness more accurately, even for individuals with limited credit histories, reducing default rates and enabling fairer lending decisions.

2. Can AI help reduce the cost of credit risk evaluation?

Yes, AI automates the labor-intensive processes of traditional credit risk assessment, such as data collection and analysis. By using predictive models and real-time data processing, microfinance institutions can save time and operational costs while delivering faster loan approvals.

3. What are the challenges in implementing AI in microfinance?

Some challenges include limited access to high-quality data, integration with existing systems, ensuring ethical AI practices, and the need for skilled personnel to manage AI systems. However, investing in robust data infrastructure and AI governance can help overcome these barriers.

4. How does AI address the needs of underbanked or unbanked populations?

AI incorporates alternative data sources such as mobile phone usage, utility payments, and social media activity to create credit profiles for individuals without formal banking histories. This enables microfinance institutions to expand financial inclusion and serve a broader customer base.

5. What role does AI play in mitigating risks for microfinance lenders?

AI-powered tools provide real-time monitoring of borrower behavior, flagging potential risks early. Predictive analytics also helps lenders identify patterns that indicate financial distress, enabling proactive interventions to prevent defaults and improve portfolio health.